May 2026: Growth holds up but inflation soars

We've teamed up with Pantheon Macroeconomics, a premier provider of unbiased, independent macroeconomic research to bring you a summary of the UK economic outlook.

- UK economic growth is holding up surprisingly well so far, in the face of higher energy prices

- More troubling news comes from rocketing inflation, as firms pass higher energy costs into retail prices

- The MPC will hold on as long as possible, but will hike Bank Rate if oil prices fail to fall back soon

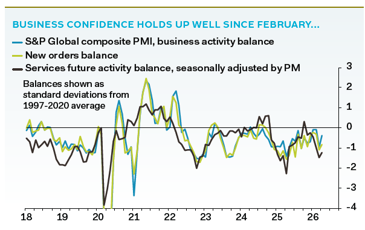

Growth is holding up surprisingly well so far

The April PMI joined a host of indicators showing that the UK economy is holding up well since oil prices rocketed after the US and Israel began bombing Iran in late February. The PMI output balance rose to 52.6 in April, from 50.3 in March and close to the long-run average for that business sentiment indicator of 54.0, as our chart below shows. New orders and confidence in future output growth also improved.

We estimate that the April PMI in isolation is consistent with 0.2% quarter-to-quarter GDP growth, which would be a more than decent result in the circumstances.

Consumers’ confidence has fallen by much less than, for instance, after Russia’s invasion of Ukraine sparked a similar surge in energy prices. Retail sales were also strong in March, house prices have kept rising, corporate borrowing growth has accelerated—usually a good sign for investment—and job growth seems to have snapped the long period of falls seen since the Chancellor hiked national insurance contributions.

Granted, some of the output gains will be temporary, resulting from firms bringing forward orders ahead of future supply disruptions. Moreover, the longer energy prices remain elevated, the more households and firms will build higher costs into their decisions, which would slow spending growth. But, for now, the growth news is surprisingly positive.

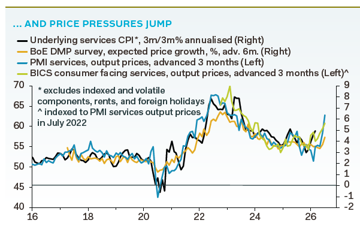

The more troubling news for the economy comes from rocketing inflation. All of the major pricing surveys we monitor show firms passing through higher energy costs into retail prices rapidly, as our chart above shows. The PMI likely exaggerates the extent to which price pressures have accelerated, but the more reliable Decision Maker Panel survey also shows a marked pickup

in inflation in April.

The MPC has to balance the impact of energy prices on growth and inflation when setting interest rates. So far, indicators point to inflation rising while growth holds up, which leaves rate setters deciding when, rather than if, to hike interest rates. Ultimately, developments in oil prices will be crucial. The MPC can avoid hiking if oil prices drop sharply soon. Otherwise, we think rate setters will have to contemplate one or two interest rate 0.25pp rate increases this year, followed by cuts in 2027.